Solar Loan Dealer Fees Explained: The Hidden Cost of Low APR

Comprehensive guide to solar dealer fees. Learn how these upfront add-ons offset advertised rates, calculate true costs, and protect yourself from hidden financing charges.

A solar dealer fee is an upfront financing cost that can inflate the system price or loan principal in exchange for a lower advertised APR. The only reliable way to spot it is to compare the cash price, financed amount, finance charge, total of payments, and any written dealer-fee disclosure.

The solar industry has perfected a deceptive financing technique that costs homeowners billions annually: the dealer fee. Hidden in complex loan structures, these fees transform seemingly attractive low-APR offers into predatory debt traps. This comprehensive guide explains what dealer fees are, how they work, and how to protect yourself from this pervasive industry practice.

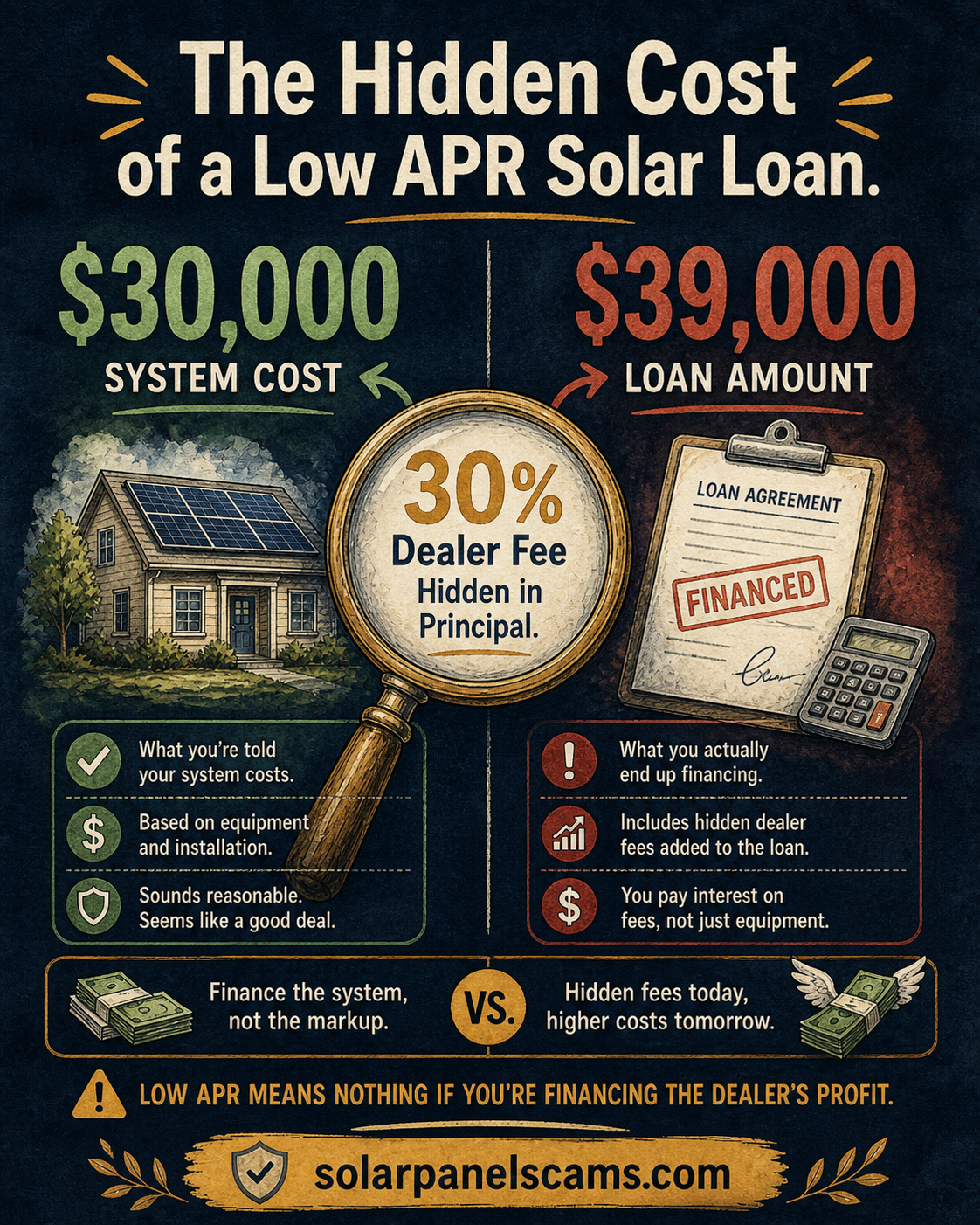

The example in the graphic is the question every homeowner should ask before accepting low APR solar financing: why is the financed amount higher than the system cost? If the cash price is $30,000 but the loan principal is $39,000, the missing $9,000 is not savings. It is usually a dealer fee or markup that you may pay interest on for decades.

What Are Solar Dealer Fees?

The Basic Concept

A "dealer fee" (also called "contractor fee," "origination fee," or "buydown fee") is an upfront charge that solar companies add to loan amounts to reduce the advertised interest rate. The fee is typically:

| Characteristic | Typical Range | Who Pays |

|---|---|---|

| Percentage of system cost | 15% - 35% | Borrower (through loan) |

| Dollar amount | $3,750 - $17,500+ | Added to principal |

| Payment method | Financed over loan term | With interest |

The Deception: Salespeople emphasize the low APR while hiding the massive fee that makes the true cost significantly higher than alternative financing options.

How the Math Works

Example: The True Cost of a "Low" APR:

| Component | Amount |

|---|---|

| System cash price | $30,000 |

| Dealer fee (30%) | $9,000 |

| Total financed | $39,000 |

| Advertised APR | 1.99% |

| Loan term | 25 years |

| Monthly payment | ~$165 |

| Total paid over 25 years | $49,500 |

| Cost vs. cash price | $19,500 more |

Alternative: Credit Union Loan:

| Component | Amount |

|---|---|

| System cash price | $30,000 |

| Dealer fee | $0 |

| Total financed | $30,000 |

| APR | 6.99% |

| Loan term | 20 years |

| Monthly payment | ~$232 |

| Total paid over 20 years | $55,680 |

| But paid off 5 years earlier | Save $8,200 in last 5 years |

The Reality: The "low APR" loan costs $19,500 more than cash—and only saves $6,180 vs. the credit union loan over the full 25 years. You're paying $19,500 extra to save $6,180.

The Mechanics of Dealer Fees

How Lenders and Solar Companies Structure These Deals

Step-by-Step Process:

Lender Sets Rate Sheet

- Base rate (no fee): 8.99% APR

- Rate with 20% fee: 5.99% APR

- Rate with 30% fee: 1.99% APR

- Rate with 35% fee: 0.99% APR

Solar Company Chooses Rate

- Lower advertised APR = higher fee = more profit

- Salespeople incentivized to push lowest APR

- Consumer focuses on rate, ignores total cost

Fee Added to Loan

- Customer finances system cost + fee

- Pays interest on fee amount for entire loan term

- Fee compounds over decades

Payment Structure

- Lower monthly payment (stretched over longer term)

- Much higher total cost

- Harder to refinance due to negative equity

Why Solar Companies Love Dealer Fees

| Benefit to Solar Company | Impact on Consumer |

|---|---|

| Higher system prices | Less price sensitivity due to focus on monthly payment |

| Faster sales | Low APR makes decision easier |

| Competitive advantage | Can advertise "1.99% financing!" |

| Higher commissions | Bigger loan = bigger dealer fee split |

| Less comparison shopping | Monthly payment focus obscures total cost |

The Incentive Misalignment: Solar company profits increase when consumers pay more. There's no incentive to offer fair financing.

The True Cost Calculator

Comprehensive Cost Comparison

Scenario: $30,000 System, Various Financing Options

| Financing Method | Total Cost | Monthly Payment | Term | Cost vs. Cash |

|---|---|---|---|---|

| Cash purchase | $30,000 | N/A | N/A | $0 (baseline) |

| Dealer fee loan (30%, 1.99%) | $49,500 | $165 | 25 yrs | +$19,500 |

| Dealer fee loan (20%, 3.99%) | $45,600 | $190 | 25 yrs | +$15,600 |

| Credit union (0% fee, 6.99%) | $55,680 | $232 | 20 yrs | +$25,680 |

| HELOC (0% fee, 7.50%) | $57,000 | $237 | 20 yrs | +$27,000 |

| Home equity loan (0% fee, 7.00%) | $55,860 | $433 | 10 yrs | +$25,860 |

Key Insight: The dealer fee loan with 1.99% APR costs $19,500 more than cash but saves only $6,180 vs. credit union over 20 years. Plus, you're locked in for 5 extra years.

Hidden Cost Multipliers

How Fees Compound Over Time:

| Fee % | Added to Principal | Interest on Fee (25 yrs at 4%) | Total Fee Cost |

|---|---|---|---|

| 15% | $4,500 | $3,000 | $7,500 |

| 20% | $6,000 | $4,000 | $10,000 |

| 30% | $9,000 | $6,000 | $15,000 |

| 35% | $10,500 | $7,000 | $17,500 |

The Long-Term Impact: A 30% dealer fee on a $30,000 system doesn't just cost $9,000—it costs $15,000 when you include 25 years of interest on that fee.

Red Flags: Spotting Dealer Fee Deception

During the Sales Process

🚩 Immediate Warning Signs:

| Statement | What It Means | Your Response |

|---|---|---|

| "1.99% APR!" | Probably 25-35% dealer fee | "What's the total amount I'm financing?" |

| "No money down" | Fee buried in loan | "What is the cash price vs. financed amount?" |

| "Special financing today only" | Prevents comparison shopping | "I need 48 hours to compare options" |

| "This won't affect your credit much" | Large loan hidden | "How is this reported to credit bureaus?" |

| "Everyone qualifies" | Predatory terms | "What are the qualification requirements?" |

In Loan Documents

🚩 Document Red Flags:

| Issue | What to Look For | Why It Matters |

|---|---|---|

| Financed amount > cash price | Loan is $39,000 for $30,000 system | Hidden $9,000 fee |

| APR vs. interest rate discrepancy | Different numbers in different places | Confusion tactic |

| Vague fee descriptions | "Finance charges," "service fees" | Obscuring dealer fee |

| No TILA disclosure | Missing required federal disclosures | Violation, red flag |

| Prepayment penalties | Charges for paying off early | Trapping you in bad loan |

Questions That Reveal the Truth

The Essential Four:

"What is the exact cash price for this system?"

- Get it in writing

- Compare to market rates

"What is the total amount I will be financing?"

- If higher than cash price, ask why

- Get fee percentage

"What is the dealer fee percentage and dollar amount?"

- If they say "no dealer fee," verify financed amount equals cash price

- If financed amount is higher, there IS a fee

"What would my total cost be with a credit union loan at their current rate?"

- Forces comparison

- Reveals true cost difference

Legal Protections and Violations

Truth in Lending Act (TILA) Requirements

What Lenders Must Disclose:

| Required Disclosure | Purpose | Common Violations |

|---|---|---|

| Annual Percentage Rate (APR) | True cost including fees | Misleadingly low APR hiding fees |

| Finance charge | Total dollar cost of credit | Not including dealer fee |

| Amount financed | Net amount provided to you | Including dealer fee in calculation |

| Total of payments | Sum of all payments | Not accounting for fee impact |

| Payment schedule | Amount and timing of payments | Hiding escalators or balloons |

Your Rights Under TILA:

- Right of rescission (3 days for home equity loans)

- Right to clear disclosures

- Right to accurate advertising

- Right to sue for violations (actual damages, statutory damages, attorney fees)

State Consumer Protection Laws

Deceptive Trade Practices:

| Violation | Remedy | Timeline |

|---|---|---|

| Hidden fee not disclosed | Rescission, damages | Varies by state |

| Misrepresented loan terms | Full refund + penalties | 2-4 years |

| Bait-and-switch pricing | Contract cancellation | Varies by state |

Better Alternatives to Dealer Fee Loans

Option 1: Credit Union Solar Loans

Advantages:

- No dealer fees

- Transparent pricing

- Member-owned (not profit-maximizing)

- Often lower total cost despite higher APR

Typical Terms:

- APR: 5.99% - 8.99%

- Term: 10-20 years

- No prepayment penalties

- Simple interest

Option 2: Home Equity Loans/HELOCs

Advantages:

- Often tax-deductible interest (consult tax advisor)

- No dealer fees

- Established relationship with lender

- Flexibility in terms

Considerations:

- Secured by home (risk if default)

- Closing costs may apply

- Requires home equity

Option 3: Cash Purchase

The Best Financial Option:

- Lowest total cost

- Full ownership day one

- All tax credits retained

- No financing complications

How to Make It Work:

- Save for 1-2 years before purchasing

- Reduce system size to match budget

- Consider phase 1 now, phase 2 later

Option 4: Solar-Specific Lenders (Fee-Free)

Some lenders offer:

- True 0% dealer fee options

- Slightly higher APR but transparent

- Better total cost than fee-laden alternatives

Examples:

- Certain credit unions

- Some regional banks

- Specialized solar lenders (verify fee structure)

How to Protect Yourself

The Comparison Shopping Rule

Always Compare These Options:

| Source | What to Get | Key Metric |

|---|---|---|

| Solar installer financing | Full loan disclosure | Total cost including fees |

| Your credit union | Solar loan quote | APR and total payments |

| Your bank | Personal loan quote | APR and origination fees |

| Online lenders | Rate comparison | Total cost of borrowing |

The 48-Hour Rule

Never Sign Solar Financing Same Day:

- Day 1: Get all quotes, read all documents

- Day 2: Calculate total costs, compare options

- Day 3+: Make informed decision

Why It Matters: Dealer fee loans look attractive initially. Time allows clear-eyed analysis of true costs.

Documentation Checklist

Before Signing:

- Cash price in writing from 3+ installers

- Total financed amount clearly stated

- Dealer fee percentage explicitly disclosed

- TILA disclosure provided

- Comparison with alternative financing

- Prepayment terms verified

- Credit reporting treatment confirmed

- All promises in writing

If You've Been Victimized

Immediate Steps

If You Just Signed (Cooling-Off Period):

- Cancel immediately (certified mail)

- Stop payment if possible

- Document everything

- Most states: 3-7 day cancellation rights

If You've Been Paying:

- Calculate total excess cost vs. fair alternatives

- Gather all loan documents

- Document any misleading statements

- Consult consumer protection attorney

Legal Options

Potential Claims:

| Violation | Remedy | Evidence Needed |

|---|---|---|

| TILA violation | Rescission, damages | Disclosure errors |

| Deceptive trade practices | Refund, penalties | Misleading statements |

| Breach of contract | Damages | Contract violations |

| Unconscionability | Contract void | Grossly unfair terms |

Where to Complain:

- State Attorney General (consumer protection)

- CFPB (lending violations)

- State contractor board (installers)

- Better Business Bureau

The Industry's Future

Regulatory Trends

Expected Changes:

| Proposal | Status | Impact |

|---|---|---|

| Fee percentage caps | Proposed in some states | Would limit to 15-20% |

| Enhanced TILA enforcement | CFPB priority | Better disclosure compliance |

| Standardized solar loan disclosures | Industry discussion | Easier comparison shopping |

| APR calculation reforms | Under consideration | More accurate cost representation |

Consumer Education Imperative

What's Needed:

- Clear disclosure of total cost vs. APR

- Standardized loan comparison tools

- Mandatory cooling-off periods

- Enhanced enforcement of existing laws

Key Takeaways

- Dealer fees are hidden wealth extraction: Often 20-35% of system cost

- Low APR is a distraction: Total cost matters, not monthly payment

- Credit unions often better: Higher APR but no hidden fees

- Calculate true total cost: Over full loan term, not just monthly payment

- Never sign same day: 48 hours minimum for review

- Get everything in writing: Verbal promises mean nothing

- Know your rights: TILA, state consumer protection laws

- Compare alternatives: Always shop multiple financing sources

Bottom Line: Solar dealer fees transform legitimate financing into predatory lending. Your protection is comparison shopping, careful calculation of total costs, and refusal to sign until you fully understand every dollar you'll pay. The "low APR" you're offered may be the most expensive money you ever borrow.

Official Sources on Solar Financing Disclosures

- The CFPB's solar financing issue spotlight describes solar loan dealer fees, payment shocks, and risks in third-party solar financing: CFPB solar financing issue spotlight.

- The Truth in Lending Act requires key credit disclosures, including finance charge, APR, amount financed, total of payments, and payment schedule: TILA disclosures statute.

- The Department of Energy explains the difference between solar loans, leases, PPAs, and cash purchases: DOE homeowner's guide to solar financing.

- The FTC warns that solar sellers should not misrepresent financing terms, costs, savings, rebates, or tax credits: FTC business guidance on solar scams.

- The CFPB complaint portal is the federal intake path for lending, servicing, debt collection, and credit reporting issues: CFPB complaint portal.

FAQ

What is a solar dealer fee?

A solar dealer fee is an upfront financing charge used to buy down the advertised APR. It is often baked into the system price or loan principal, which makes the loan look cheap monthly while quietly making the system more expensive.

Are solar dealer fees illegal?

Not automatically. The problem is nondisclosure or misleading presentation. If the salesperson sells the loan as a bargain rate without explaining the inflated principal, the pitch can cross into deceptive financing.

How do I spot a hidden dealer fee?

Ask for the cash price, the financed price, the dealer fee percentage, and the total of payments. If the financed amount is thousands higher than the cash price, the "low APR" probably has a fee hiding behind it.

Is a higher APR loan sometimes cheaper than a low APR solar loan?

Yes. A no-fee credit union loan can cost less overall than a low APR solar loan with a huge dealer fee. Compare total cost over the whole term, not just monthly payment.

What should I do if the dealer fee was hidden from me?

Save the contract, TILA disclosures, proposal, texts, and screenshots, then compare the loan against the dealer fee breakdown guide and solar financing scams guide. If the numbers do not reconcile, consider a consumer-protection attorney.

Related Reading

- Solar Financing Scams: Complete Guide

- Truth in Lending Act Rights

- Credit Union vs. Solar Financing Comparison

Last updated: 2026-06-20. Calculate total costs carefully before committing to any solar financing.

Got blindsided by a solar deal that did not deliver?

You may have a claim — and the law may make the company that defrauded you pay your legal fees. Our 2-minute eligibility check screens for the consumer-protection statutes that apply to your situation (TILA § 130, the FTC Holder Rule, your state UDAP) and connects you with a consumer-protection attorney in our network if you qualify. Use the eligibility form to route your facts through the right intake path.

Next Research Steps

Use these resources to connect this issue with the broader solar scam pattern, the relevant legal framework, and the next practical action.

Solar panel scams

Start with the main solar panel scams guide for the broad definition and recovery roadmap.

Solar financing fraud compensation

Use this guide for loan, dealer-fee, payment-jump, PACE, lease, and lender-defense issues.

Homeowner legal rights

Review cancellation, rescission, UDAP, TILA, Holder Rule, arbitration, and lawsuit options.